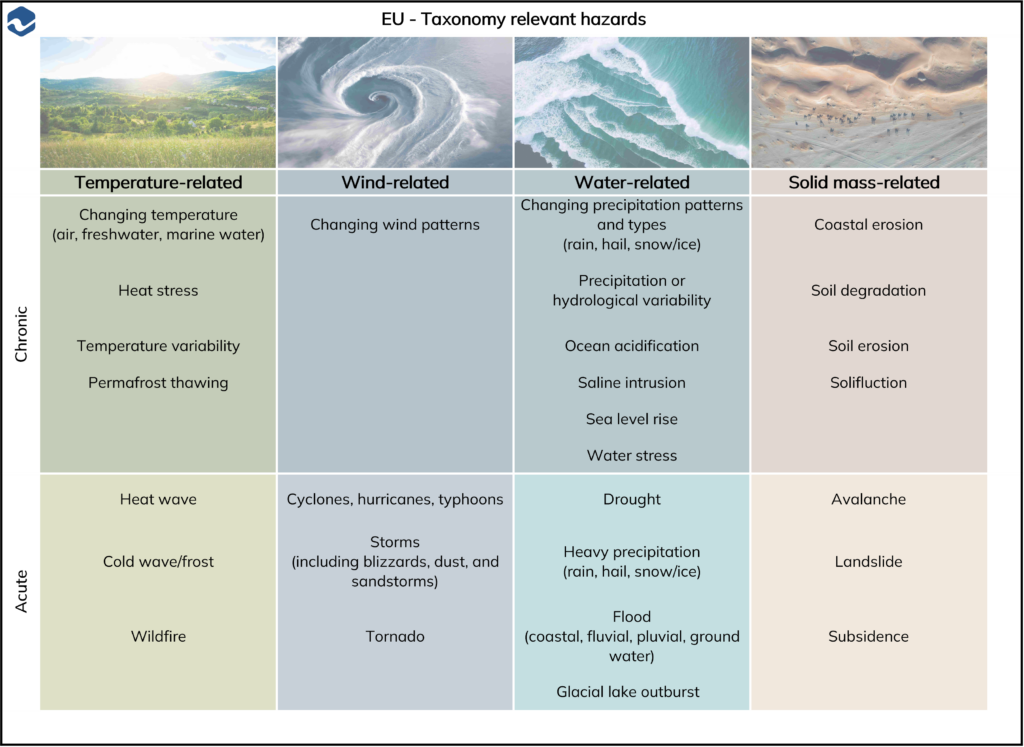

| EU – Taxonomy relevant hazard | ||||

|---|---|---|---|---|

| Chronic | Temperature-related | Wind-related | Water-related | Solid mass-related |

|  |  |  | |

| Changing temperature (air, freshwater, marine water) | Changing wind patterns | Changing precipitation patterns and types (rain, hail, snow/ice) | Coastal erosion | |

| Heat stress | Precipitation or hydrological variability | Soil degradation | ||

| Temperature variability | Ocean acidification | Soil erosion | ||

| Permafrost thawing | Saline intrusion | Solifluction | ||

| Sea level rise | ||||

| Water stress | ||||

| Acute | Heat wave | Cyclones, hurricanes, typhoons | Drought | Avalanche |

| Cold wave / front | Storms (including blizzards, dust, and sandstorms | Heavy precipitation (rain, hail, snow/ice) | Landslide | |

| Wildfire | Tornado | Flood (coastal, fluvial, pluvial, ground water) | Subsidence | |

| Glacial lake outburst | ||||